Abstract

Japan’s bond market is undergoing a structural transition from central bank-driven pricing to market-driven pricing. The core driver of rates has shifted toward a reconstruction of risk compensation mechanisms. As the BOJ proceeds with Quantitative Tightening (QT), duration risk is being reintroduced to private balance sheets. Simultaneously, the U.S.-Iran conflict acts as a “Bad Inflation” catalyst, eroding Japan’s terms of trade. This combination creates a fragile equilibrium where yields are prone to nonlinear jumps, and domestic capital repatriation threatens to tighten global financial conditions.

Evolution of Core Logic: From Policy Intervention to Risk Compensation

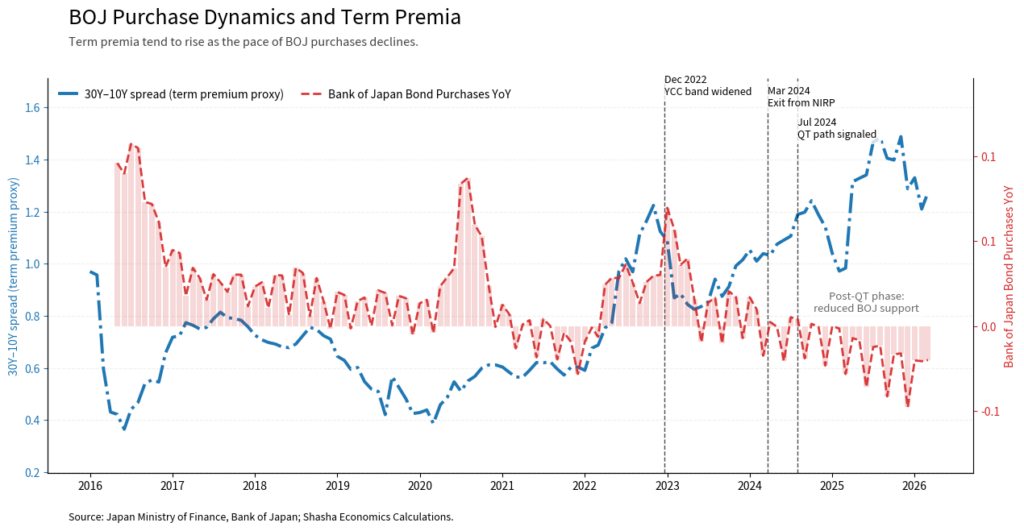

During the intensification phase of quantitative easing, the central bank compressed the effective supply of long-term bonds through large-scale purchases, systematically suppressing the term premium. However, as the pace of bond purchases has slowed or even stalled in recent years, the market has been forced to reabsorb duration risk, leading to a rebound in the term premium. This mechanism has become particularly evident since 2022, reflecting a transition in the Japanese bond market from “BOJ-set pricing” to “market-based pricing.”

Looking at the relationship between BOJ bond purchases and term spreads, as the year-on-year growth rate of purchases has trended toward zero, the spread between 30-year and 10-year yields has widened significantly. This indicates that in the absence of continuous central bank buying, investors are demanding higher risk compensation for long-term bonds. During the Yield Curve Control (YCC) era, the BOJ effectively suppressed long-end yields through persistent intervention. That pricing anchor is now fading, and the market is rebuilding the pricing framework for long-term rates.

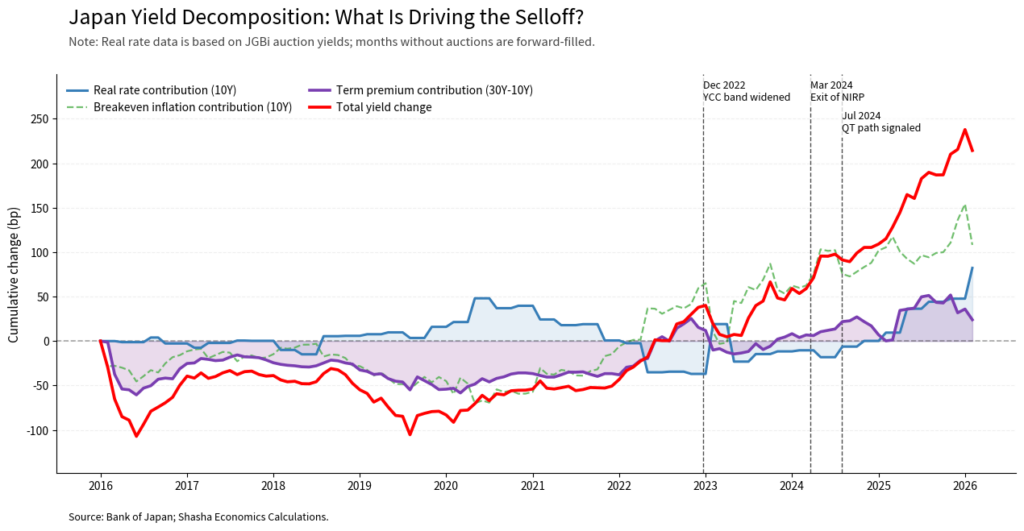

From the perspective of yield decomposition, past rate increases were mostly driven by inflation expectations or growth improvements. In contrast, while inflation expectations still retain explanatory power, recent increases in Japanese rates have increasingly reflected a repricing of the term premium. This implies that the current rise in interest rates is not a typical “fundamentals-driven” increase but rather a repricing process for uncertainty and risk.

Curve Morphology: Long-End-Led Bear Steepening

At the short end, as the BOJ exits its negative interest rate policy, real rates are gradually moving out of deeply negative territory. This not only raises the short-term rate floor but also transmits upward pressure to the mid-to-long end via arbitrage relationships. At the same time, inflation uncertainty stemming from external energy shocks is further pushing up yields at the margin.

However, the dominant force shaping the yield curve in this cycle comes from the long end. The normalization of the term premium, combined with geopolitical risk premia, has caused 30-year yields to rise more sharply than intermediate maturities, resulting in a classic bear steepening of the yield curve.

This structural shift implies that market pricing has moved away from being centered solely on the policy path, toward a broader framework of risk compensation. In other words, interest rates are no longer merely a reflection of policy expectations, but a comprehensive pricing of tail risks, liquidity risks, and uncertainty.

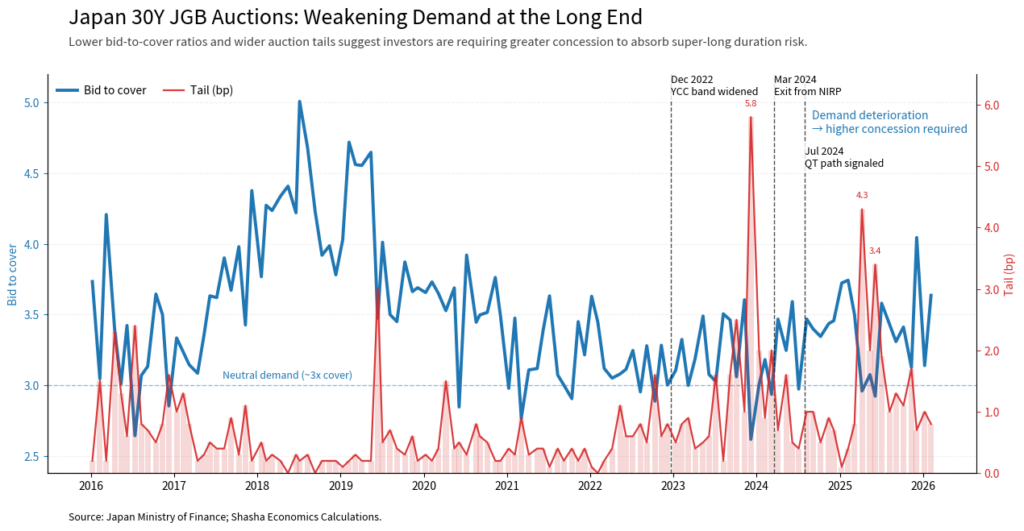

Micro-Evidence: Auction Tails Reveal Intrinsic Fragility

Primary market dynamics provide more direct evidence of this transition. Auction data for 30-year government bonds show that during the policy transition phase since 2024, auction tails have frequently experienced widening.

More notably, in certain auctions, the bid-to-cover ratio did not deteriorate significantly, yet the tail widened markedly. This combination of “stable quantity, deteriorating price” reveals a critical shift: marginal demand is rapidly weakening. The market does not lack participants, but rather, buyers are only willing to accept supply at higher yield levels. Price sensitivity has risen significantly, and market depth has noticeably declined.

Such a structure suggests that the market appears to maintain demand on the surface, but has in fact entered a state of fragile equilibrium. Once supply or policy shocks intensify, interest rates may experience non-linear jumps.

External Shocks: U.S.-Iran Conflict and the “Bad Inflation” Policy Paradox

The escalation of the U.S.-Iran conflict is reshaping the external environment. The current oil price shock is a classic form of “bad inflation,” which arises from deteriorating terms of trade rather than endogenous demand expansion.

For Japan, this shock directly erodes corporate profits and household real income by raising energy import costs, thereby suppressing demand while pushing up inflation. This creates a “divergence” between inflation and growth, making policy transmission mechanisms far more complex.

This has important policy implications. If the BOJ raises interest rates to combat energy-driven inflation, it is essentially implementing demand-contraction policies in response to a supply shock. This could exert additional pressure on an economic recovery that is not yet solidified. Therefore, the current rise in inflation does not necessarily imply greater room for monetary tightening. Instead, it reinforces policy constraints and increases the complexity of policy trade-offs.

At a deeper level, the shift in interest rate structures is creating spillover effects through cross-border capital flows. For over a decade, Japan’s negative real rate environment made institutional investors “go abroad” in search of yield, allocating to U.S. Treasuries and other overseas assets.

However, as domestic real rates recover, the relative attractiveness of Japanese assets is improving, and capital repatriation pressure is beginning to emerge. Once this process unfolds, its impact will extend beyond Japan. As one of the world’s largest net external investors, Japan’s marginal reallocation of capital may weaken demand for U.S. Treasuries and other global assets and exert upward pressure on global yields.

Conclusion and Outlook

The core of the current rise in Japanese interest rates is not traditional growth or inflation dynamics, but a systematic reconstruction of risk compensation mechanisms. The normalization of the term premium is the main driver, while the oil shock acts as an amplifier by increasing uncertainty and accelerating the repricing process.

Looking ahead, the yield curve is likely to continue exhibiting a long-end-led upward trend. Short-end rates will rise gradually, supported by improving real rates, while long-end yields will maintain stronger upward momentum under the combined influence of term premia and geopolitical risk premia.

Key risks lie in market liquidity. Persistent widening in auction tails suggests limited marginal absorption capacity. In an environment of ongoing QT, increased supply, and policy uncertainty, the risk of nonlinear amplification in yield volatility is rising.

At the same time, the potential for capital repatriation should not be underestimated. If Japanese investors reduce their overseas bond allocations, this could have a lasting impact on global interest rates and reinforce the tightening of global financial conditions.